Secured Debt Consolidation Loans For Bad Credit UK Direct Lender

There is a rush to lend as interest rates decline, and lenders are even betting on lower rates. UK wages are often strong, and unemployment is very low.

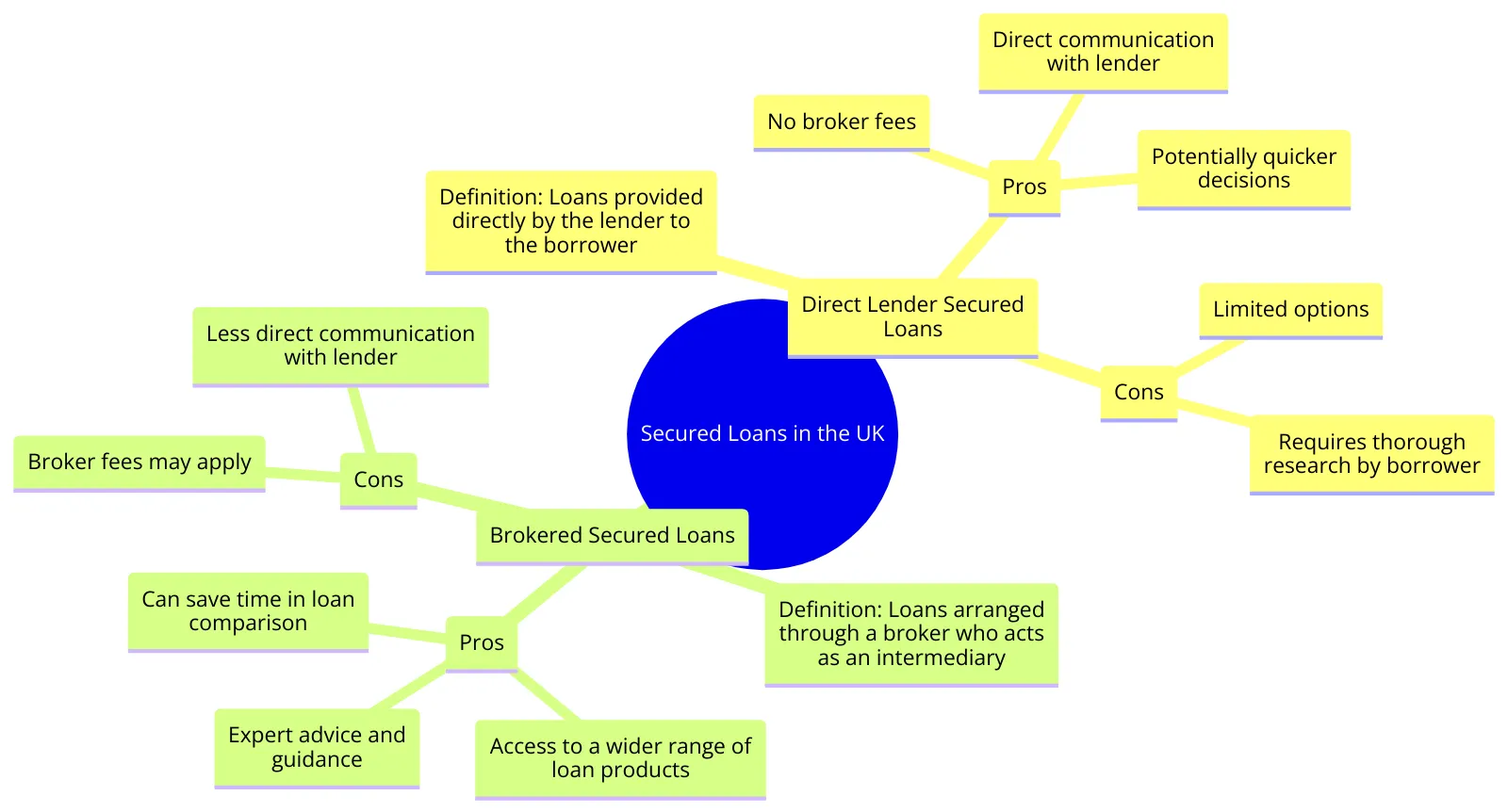

1st UK Mortgages has a new direct lender, Fund Fortress, for secured debt consolidation loans, not featured on the comparison sites, backed by funds from Hong Kong investors.

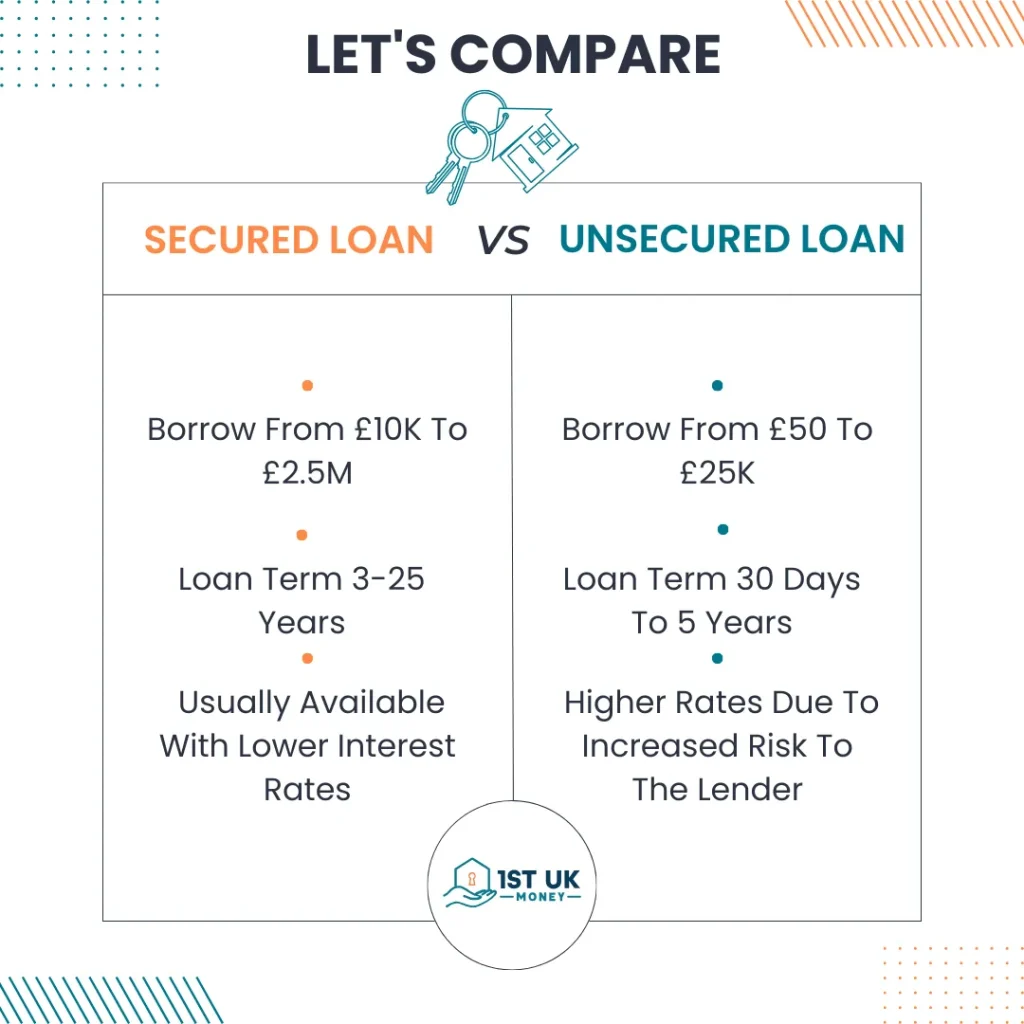

If you want to borrow money to improve your home for a loft conversion or extension, you can access the assumed home valuation when the works have been completed.

Here Are Some Of The Key Features On Offer:

- Ideal for debt consolidation

- Overall loan-to-value up to 90%

- No lender, broker or adviser fees

- Fixed for life rate of 6.76% APR

- No upper or lower age limit

- Up to one penalty-free payment holiday a year

- Free no obligation home valuation

- No penalty for flats or other leasehold properties

- Open minded view on affordability and credit score

- No early repayment charges/redemption penalties

Enter Some Details In Our Quick & Simple Form. Soft-Search Technology

Why should I consolidate my debts in 2026?

Simplicity

A secured debt consolidation loan will be debited from your bank account once a month, and can be debited just after your payday. This makes your life and budgeting very simple.

If you had a personal loan, a store card, two credit cards, and a consumer credit agreement for a sofa, all due at different times of the month, your finances could be messy.

Not everyone is great at managing money. This makes missed or late payments more likely.

Dealing with debt and paying it down for good

Having credit cards and being trapped into paying the minimum each month can be challenging to escape. Paying down cards a bit, then running them back up throughout the month, makes your debt look like an interest-only loan.

Paying off your credit cards and store cards with a debt consolidation secured loan will force you to not only service the debt but also pay down the principal each month, so eventually, the debt will go away, which is what you should want.

Being in debt for many years could eventually affect your standard of living in retirement.

What are the drawbacks of secured debt consolidation loans?

Secured debt consolidation loans offer advantages, including lower interest rates and the potential to consolidate multiple debts into a single, manageable payment.

However, they also come with several drawbacks that borrowers should carefully consider:

- The loan is secured on your home

- A longer loan term can drag out the total amount of interest paid

- Lenders are very fussy about the borrower’s income and other circumstances

If you have too much debt, you may want to consider a Step Change.

Can you get a secured loan for debt consolidation?

Yes, it’s easy to get a secured loan for debt consolidation as long as you have the income to support it.

Is a secured loan a good idea for debt consolidation – to make debt easier?

It can be an excellent idea as it can save you money each month.

Do debt consolidation loans hurt your credit?

No, in many cases, quite the opposite, as they help you pay debt down.

How hard is it to get a debt consolidation loan?

Getting a debt consolidation loan is easy if you can prove your income to the lender at the right level.