Pensioner Mortgages For 60, 65, 70, Or 80-Year-Olds

1st UK Mortgages specialises in pensioner mortgages and later-life borrowing. We can often help where standard lenders are limited by age, term or affordability rules. Rates can start from 4.2%, and selected plans may allow borrowing of up to 60% of your home’s value.

GREAT LOW MARKET RATES FOR OVER 55’S

GREAT CHOICE, STRAIGHTFORWARD APPLICATIONS

A growing number of over 55’s are looking for a mortgage because:

- They have an existing mortgage they want to repay or replace

- They want to release money for retirement, family support or home improvements

Over 55’s have a choice of 3 types of mortgages to meet their needs:

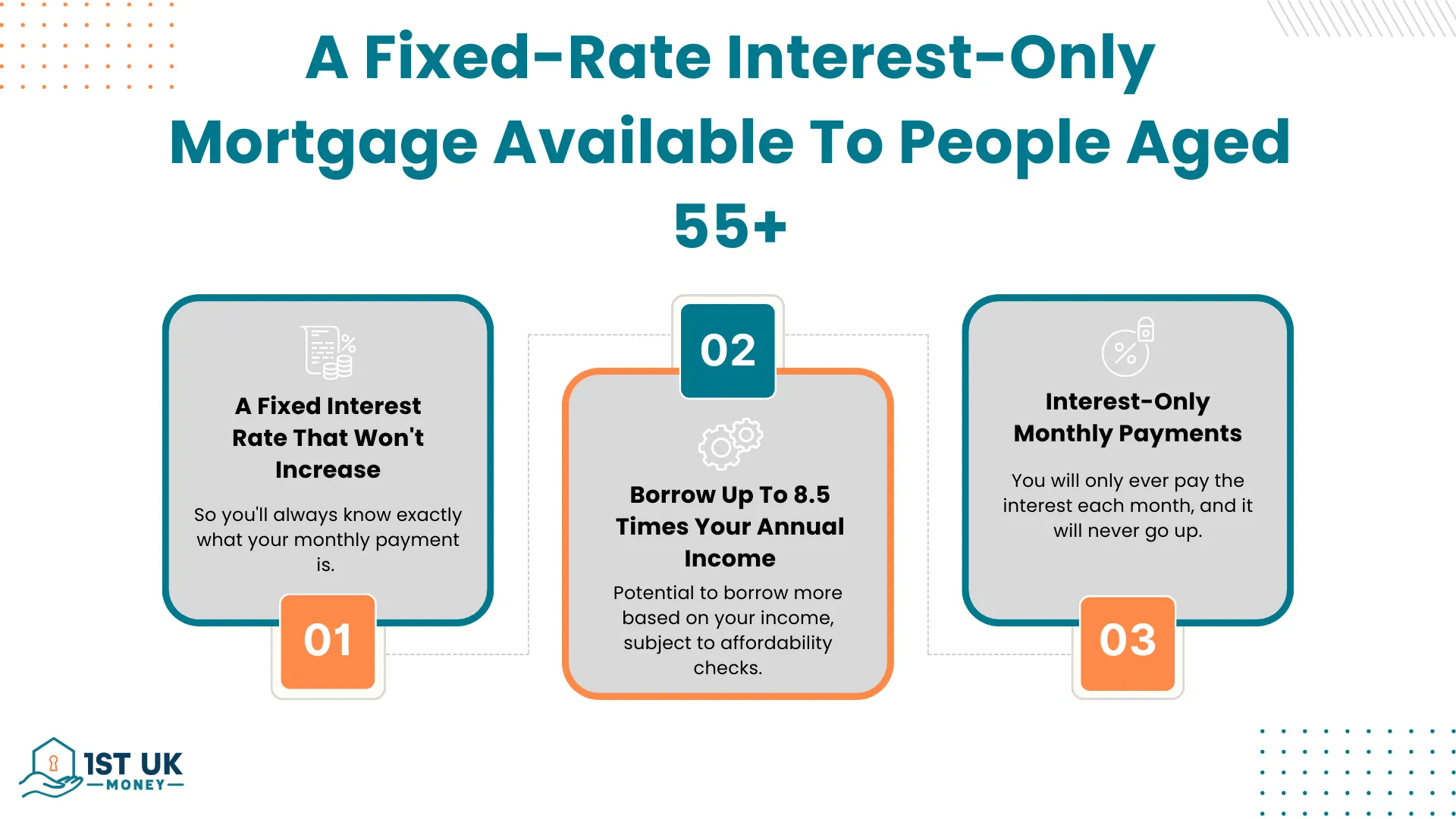

- A lifetime mortgage can allow no monthly repayments, voluntary payments or full interest payments, depending on the plan.

- A fixed-term retirement mortgage works more like a standard mortgage, with monthly capital and interest payments.

- A Retirement Interest-Only Mortgage, often called a RIO, requires monthly interest payments but usually no fixed end date.

Please Complete The Form Below For Your Decision In Principle:

Many older homeowners need a mortgage after 60 because an existing loan is ending, an interest-only balance remains unpaid, or they want more flexibility in retirement. 1st UK Mortgages focuses on plans that can be serviced from pension income, including RIO mortgages and lifetime mortgages.

We also work with specialist lenders that are not usually shown on comparison websites. Their criteria are designed for older borrowers and can offer competitive rates, no upper age limit and simple application routes.

Lender 1: Up to 55% loan to value

- Free no obligation home valuation

- 4.89% Fixed for life

- Interest-only payments

- Up to two penalty free payment holidays a year

- No lender, broker, or advisor fees

- All applicants must be over 55 years old at the time of application

- No upper age limit or fixed mortgage term

Lender 2: Up to 65% loan to value

- 5.12% Fixed for life

- Free no obligation home valuation

- Interest-only payments

- Up to two penalty free payment holidays a year

- No lender, broker, or advisor fees with this lender

- All applicants must be over 55 years old at the time of application

- Criteria tailored to older borrower income

Mortgages For Over 60’s, 70’s and 80’s With The Following Benefits:

- Interest rates similar to conventional prime mortgage lenders

- Flexible approach to loan-to-value

- Lenders not available on price comparison websites

- Make capital repayments or just pay interest

- No maximum age limit on selected plans

- Get a tax free lump sum

- Flexible eligibility criteria for older borrower circumstances

Pensioner Mortgages FAQ’s

Can pensioners get a mortgage?

Yes. Many lenders now consider pension income, private pensions, state pension and other reliable retirement income. The right product depends on age, property value, loan size and whether you want to repay interest each month.

Is a mortgage for pensioners a good deal?

It can be, especially where rates are fixed and the monthly payment is affordable. Some older borrowers compare mainstream and specialist options, including Nationwide mortgages for over 70s, Halifax mortgages for over 70s, Nationwide mortgages for over 60s, and Saga mortgages for over 60s.

Loans for the over 75’s?

Some specialist lenders are comfortable with applicants over 75 because pension income is usually stable. This can make later-life mortgages suitable for repaying an existing mortgage, raising funds or moving home.

Mortgages In Retirement

Mortgage lenders assess whether the repayments are affordable for the term requested. A long fixed-term repayment mortgage can be difficult after 60, but RIO mortgages, lifetime mortgages and specialist retirement products may be more suitable.

Some lenders set a maximum age at application or maturity, while others have raised their limits or removed them for selected products. Nationwide was among the first high-street lenders to extend borrowing to age 85 at mortgage maturity.

About Interest-Only Retirement Mortgages For Pensioners Over 70

Older interest-only mortgages were sometimes linked to endowment policies that did not perform as expected. If that applies to you, see Dealing with an Endowment Shortfall.

Lenders have changed criteria in recent years, with some banks raising age caps because many people now work longer or retire with stable income. Barclays has accepted interest-only mortgages for over-65s with terms up to age 70 at maturity, and some mortgages for people over 50 are also available.

Nationwide Mortgages For Over 60s & 70s

Nationwide has offered residential mortgages to older borrowers with a maximum age at maturity of 85, subject to affordability and lending criteria. At age 60, this may still allow a meaningful mortgage term.

A report by The Telegraph also highlighted specialist lenders that may consider older residential mortgage applicants with more flexible age criteria.

Those include:

- National Counties Building Society

- Harpenden Building Society

- Bath Building Society

- Metro Bank

- Dudley Building Society

- The Cambridge Building Society

To compare lender criteria properly, speak with a mortgage broker who understands later-life lending. Some borrowers use a retirement interest-only mortgage to replace an expiring mortgage or consolidate borrowing, while paying the interest monthly so it does not roll up.

Interest-Only Mortgages Require A Repayment Strategy

For an interest-only mortgage, lenders usually need evidence of a credible repayment strategy. Speculating that a future sale or house price growth will cover the debt is unlikely to be enough.

Acceptable strategies can include savings, investments, pension lump sums, downsizing or other documented assets. For example, this document from Scottish Widows explains the type of evidence a lender may request. Find out more about mortgages for those 65 and over here.

It’s important to note that when you have an interest-only mortgage, lenders can ask you at any time to review and provide evidence that your repayment plan is still on track. If they feel it’s not going to be sufficient to cover the loan amount, they can ask you to change your mortgage from interest-only to another type of mortgage product that will repay the capital plus interest.

Interest-only mortgages for over-65-year-olds

A retirement interest-only mortgage may suit borrowers over 65 who can comfortably cover the monthly interest from pension income. Payments can be lower than a repayment mortgage because the capital is not repaid each month.

What If I Don’t Want To Make A Monthly Payment?

If you do not want monthly payments, a lifetime mortgage may be more suitable than a RIO mortgage. Interest can roll up, although this will usually reduce the equity left in the property.

Even if you still have a substantial balance on your current interest-only mortgage a Rio mortgage without maximum age limits at a low-interest rate can be much better than other equity release options before you die or move into long term care.

Mortgages For Pensioners FAQs

Can you get a mortgage if you are a pensioner?

Yes. Many mainstream and specialist lenders offer pensioner mortgages, subject to income, property value, loan size and affordability.

Can you get a mortgage at 70 years of age?

Yes. Some lenders offer retirement interest-only and later-life mortgage products for borrowers aged 70 and over.

What is a retirement mortgage?

It is a mortgage designed for retired or older borrowers, usually assessed against pension income and retirement affordability.

Can I get a 100% mortgage at 60?

It may be possible only with extra security, another property or additional collateral, depending on lender criteria.

Is it easy for a pensioner to get a mortgage?

It can be straightforward where income is stable and repayments are affordable, but the right lender matters.

Who offers the best mortgages for over 75s?

The best lender depends on your income, property, loan amount, age and whether you want interest-only, repayment or lifetime borrowing.

Do banks in the UK give mortgages to pensioners?

Yes. Many UK banks and building societies now consider applications from pensioners and borrowers over 70.

What is the maximum age for a Santander mortgage in the UK?

Santander criteria can depend on product type and term, so borrowers should check current rules before applying.