Secured Debt Consolidation Loans For Bad Credit From A UK Direct Lender

There is a strong appetite to lend where the case is clean enough and the property security is there. For homeowners carrying card balances, personal loans and other monthly commitments, the attraction is simple: one payment, one date, and a debt that is actually being repaid rather than shuffled around.

1st UK Mortgages has access to Fund Fortress for secured debt consolidation loans. The product is not usually seen on the main comparison sites, and it may suit borrowers who want to keep their current mortgage but tidy up expensive unsecured borrowing.

The same route can also be considered when the money is for home improvements, such as a loft conversion, an extension, or essential repairs. In some cases, the lender may take a practical view of the property value once the works have been completed.

Here Are Some Of The Key Features On Offer:

- Ideal for debt consolidation

- Overall loan-to-value up to 90%

- No lender, broker or adviser fees

- Fixed for life rate of 6.76% APR

- No upper or lower age limit

- Up to one penalty-free payment holiday a year

- Free no obligation home valuation

- No penalty for flats or other leasehold properties

- Open minded view on affordability and credit score

- No early repayment charges/redemption penalties

Enter a few details for a soft-search lending check

Why consolidate debts into one secured loan?

A secured debt consolidation loan can replace several separate payments with one monthly direct debit. That can make budgeting easier, especially where credit cards, store cards, car finance and personal loans all leave the account on different dates.

The real benefit is not just neatness. Credit cards can trap people into paying interest for years while the balance barely moves. A repayment loan forces the balance down each month. For many people, that is the part that matters.

There is still a trade-off. A lower monthly payment can be achieved by spreading the borrowing over a longer term, but that can increase the total interest paid. It only makes sense if the new loan is affordable, the old debts are cleared, and the borrower is unlikely to run up the cards again.

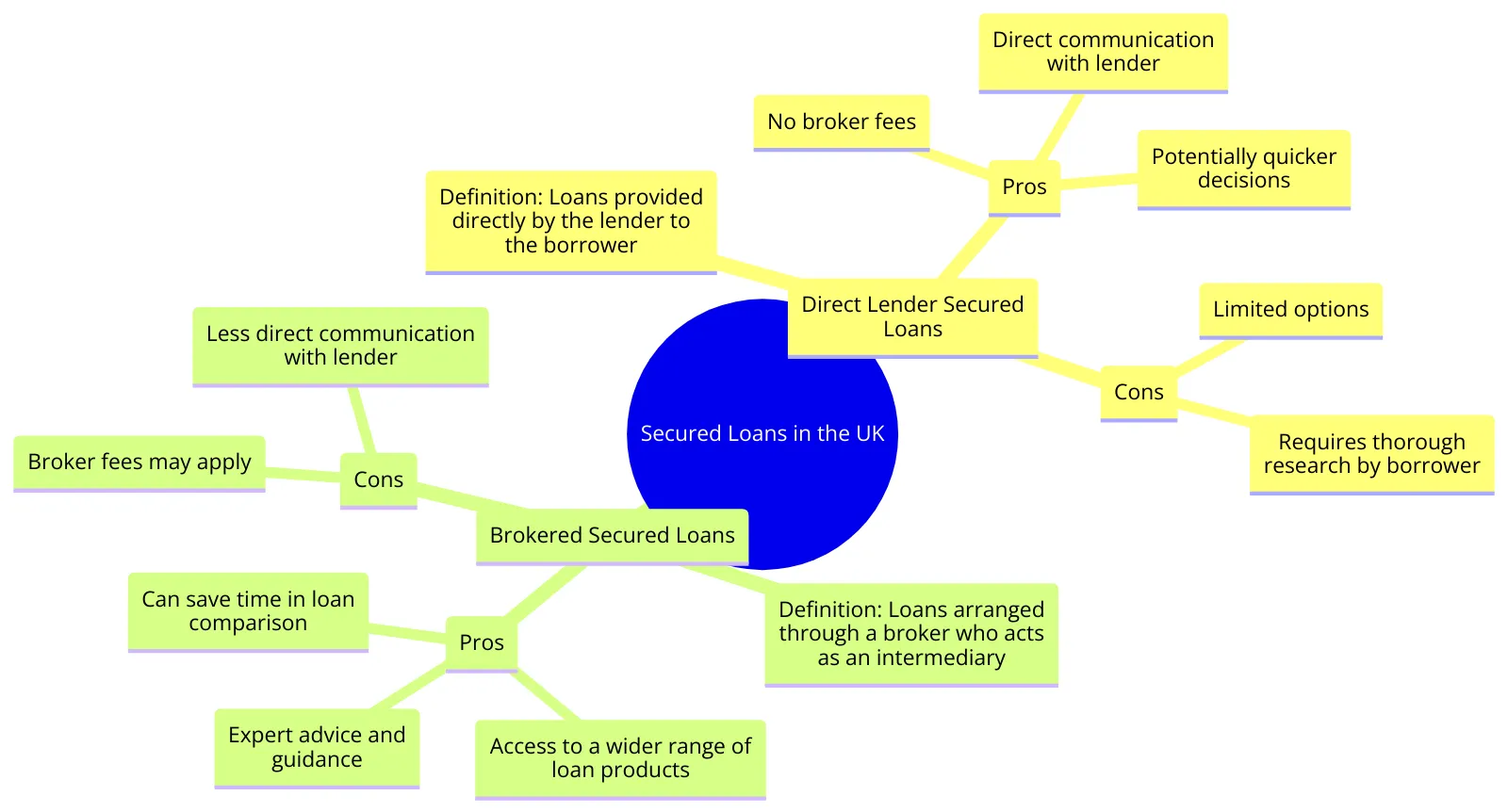

When a direct lender may not be the whole answer

Direct lending can look attractive, but the best route is not always obvious from the rate alone. Some borrowers need a lender that is comfortable with older missed payments. Others need a lender that will listen properly when income is uneven, self-employed, commission-based or split between two applicants.

That is why it can be useful to compare a direct-lender option with specialist second-charge lenders. For example, a broker might look at 1st Stop where speed and adverse credit are part of the discussion. An older-style case linked with Blemain Finance may now sit closer to the kind of lending associated with Together, while Together Money itself can be relevant when the security is strong but the circumstances need a human look.

Some lenders are more useful on heavier credit histories. Masthaven Bank has often been discussed for more complex cases, while Pepper Money can be worth reviewing where the income and credit file do not fit a standard bank. Norton Finance may also be part of the conversation where a broker wants another view before deciding whether a case is worth placing.

For borrowers with cleaner affordability, the comparison may move towards lenders such as Optimum Credit, Paragon Bank or Precise. Where the case is more about speed, property type or rate certainty, Spring Finance and United Trust Bank can give a useful benchmark.

How the loan purpose changes the lender shortlist

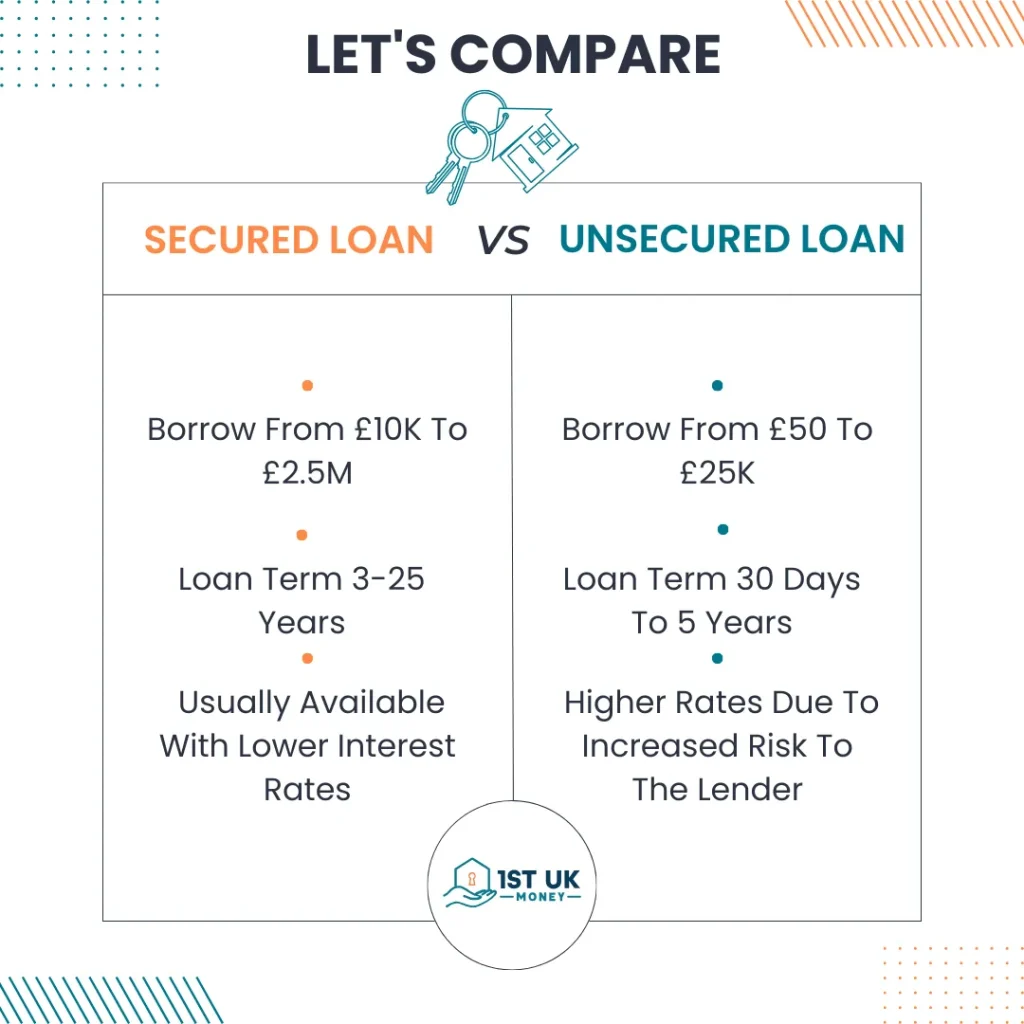

If the purpose is pure consolidation, the lender will usually want to know which debts are being repaid and whether the new monthly payment is sensible. Where the borrowing is for a large one-off job, a £25,000 loan may be enough for smaller work, but a larger secured loan could be needed for structural repairs or a proper extension.

Rate-sensitive borrowers will often ask about competitive secured loan rates, but the headline rate is only one part of the case. The same borrower may also need to look at second mortgage rates, because the product can sit behind the existing mortgage without disturbing a good first-charge deal.

Some people want certainty, so a fixed-rate secured loan may be easier to live with than a variable product. Others prefer a shorter route out of debt, and a secured loan over ten years can feel more disciplined than stretching the borrowing over a much longer term.

Credit history changes the whole tone of the application. A homeowner with recent defaults may need a lender used to bad-credit homeowner loans, or a product designed around secured loans with bad credit. A couple applying together may also get a better outcome from a joint secured loan, provided both incomes are stable enough to support the borrowing.

Not everyone wants long calls before they know whether the figures work. In that situation, a secured loan with no phone calls can be a calmer starting point, although a proper discussion may still be needed before any lender issues a binding offer.

Home improvement borrowing and high-street alternatives

Debt consolidation is not the only reason to release money from a property. Some borrowers use the funds for repairs, extensions, family needs or other practical expenses. The page about the uses of a secured loan gives a wider view of how the money might be used once the lender is happy with the purpose.

Borrowers with strong credit may not need a specialist lender at all. A clean case might be compared with NatWest home improvement loans, while a homeowner who prefers a building society may want to check Nationwide home improvement loans. For some borrowers, Santander home improvement borrowing or TSB secured loans may be a better comparison than an adverse-credit lender.

What are the drawbacks?

Secured debt consolidation can reduce monthly pressure, but the loan is secured on your home. If payments are missed, the consequences can be far more serious than missing a credit-card payment.

However, they also come with several drawbacks that borrowers should carefully consider:

- The loan is secured on your home.

- A longer term can increase the total interest paid.

- Lenders will still look closely at income, credit history and affordability.

If the debts are already unmanageable, it may be better to speak to StepChange before taking on more secured borrowing.

Can you use a secured loan for debt consolidation?

Yes. Homeowners often use a secured loan to clear credit cards, personal loans and other borrowing, provided the new payment is affordable, and the lender is happy with the case.

Is debt consolidation always the cheapest answer?

No. It can reduce the monthly payment, but a longer term can mean more interest overall. It depends on the rate, the term, the debts being repaid and whether the borrower will avoid running the cards up again.

Will a debt consolidation loan affect my credit file?

The application, repayment record and any soft or hard credit searches can all matter. Paying debts down properly can help, but missed payments on the new loan would cause problems.

How hard is it to get a debt consolidation loan?

It depends mainly on income, affordability, property value, mortgage balance and credit history. Some specialist lenders will consider cases that a high street bank would not want.