The Uses Of A Secured Loan – From 6.8% No Broker Fees

A secured loan is usually taken against a property you own. People use this type of borrowing for all sorts of reasons: repairs that cannot wait, work on the house, paying off expensive credit, buying something costly, or investing in a business. It can allow a larger loan than an unsecured option, but it is not light borrowing. If the repayments are missed, the property used as security can be at risk.

Because the lender has security, the monthly cost may look more manageable than a shorter unsecured loan. That does not make it cheaper in every case. A long term can keep the monthly payment down while making the total amount repaid much higher. That is why the purpose of the loan matters as much as the advertised rate.

A broad specialist lender panel with secured loan products and high acceptance rates

- Match the term of your loan to the remaining term of your mortgage

- Useful for clearing other loans, credit cards or existing car credit

- New lenders for 2026 now available

- High loan-to-value options with many lenders

- Same day decisions where the case is straightforward

- Retain your existing mortgage where that suits the case

- Soft footprint credit search that will not affect your credit score

- Rates from 6.8%, subject to status and lender criteria

- Borrowing can reach high loan-to-value levels where the case fits

- No pressure to proceed

Pre-decision form for homeowners with clean, light or damaged credit

Before deciding what the loan is for

Most secured loans are used for practical things rather than day-to-day spending. Home improvements, expensive repairs, debt consolidation and large purchases are common reasons. Some borrowers look at rolling several debts into one secured repayment, while others are trying to fund a room, roof, driveway, extension or other work that would be hard to pay for from savings.

If the job is house-related, it is worth comparing the secured-loan route with lender-specific home-improvement routes. Some borrowers look at Nationwide-style home improvement borrowing, others compare NatWest home improvement loan options or a Santander home improvement loan. The right answer can depend on the existing mortgage, equity, income and credit file.

What people use secured loans for

A secured loan can be used for a kitchen, bathroom, loft conversion, extension or urgent repair. It can also be used for a car, wedding, family cost or other large one-off purchase. Borrowing against a home for a short-lived purchase warrants some thought, because the loan may outlast the item being paid for.

Debt consolidation is another common reason. The monthly payment can fall if several credit cards or loans are cleared into a longer secured loan, but the total interest can rise if the new loan runs for many years. A borrower with past missed payments may still be able to secure a bad-credit homeowner loan or a secured loan when the credit file is messy, but affordability still has to make sense.

Some people borrow a specific figure rather than start with a lender. If the target is around £25,000 for a planned cost, the choice among unsecured lending, a secured loan, and further mortgage borrowing can look quite different from that in a much larger case. For longer borrowing, a ten-year secured loan term may be a good middle ground: not very short, but not stretched to the longest term either.

Borrowing for business or property plans

Secured loans are sometimes used for business purposes. That may mean buying equipment, covering a trading gap, expanding a small operation, or raising money against a residential property when the business itself lacks sufficient security. It is a different conversation from borrowing for a kitchen or clearing cards, because the repayment depends on how stable the business income is.

Property investors may use secured borrowing for deposits, repairs, auction work, or to move quickly on another opportunity. It can be useful, but it can also make a later remortgage more awkward, because another lender will see the extra secured debt. Some borrowers compare this with remortgage deals if the current mortgage is no longer tied in.

Secured and unsecured borrowing

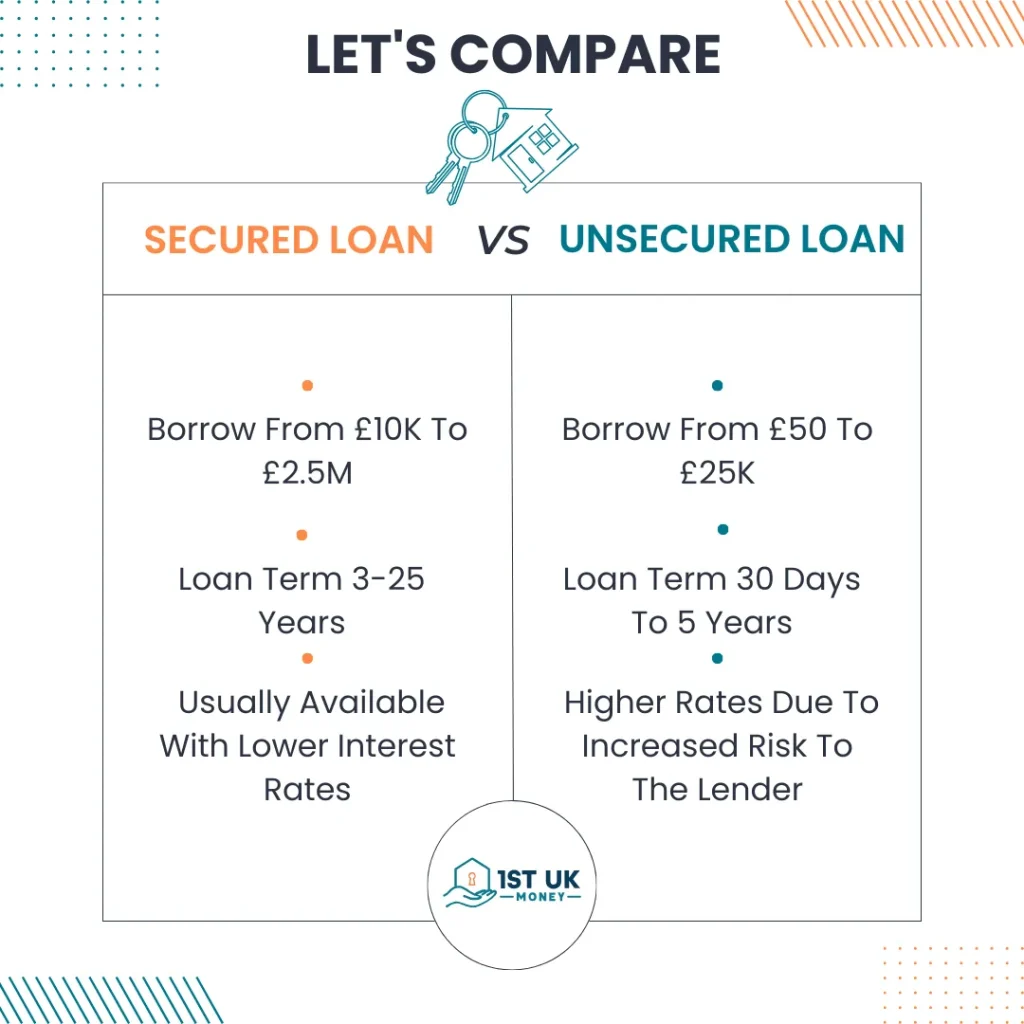

A secured loan is different from an unsecured personal loan because the lender takes security over an asset, usually the borrower’s home. That security can mean a larger loan, a longer term and a lower rate than some unsecured products. The trade-off is simple enough: if the loan is not paid, the home is part of the risk.

There are different ways to compare the loan. Some people start with the secured loan rate they might qualify for, while others look first at the second mortgage rates available for their LTV. A fixed-rate secured loan can appeal to someone who wants the payment to stay steady, while a variable rate might suit a different case.

How the lender looks at the case

The lender will usually want details of income, mortgage balance, credit commitments and the value of the property. Employed borrowers may be asked for payslips or a P60. Self-employed borrowers may need bank statements, tax calculations, and accounts. The process can be quick in a clean case, but valuations, credit issues or unusual income can slow it down.

A single borrower may qualify on their own income, but there are cases where a joint secured loan application gives the lender a fuller affordability picture. Some borrowers also ask for a quieter application with fewer phone calls, especially where they are only checking what might be possible.

Comparing lenders without turning it into a link farm

Different lenders are better at different cases. A borrower with unusual income might compare the Precise second-charge route with Pepper Money for adverse-credit cases. A more specialist property or income story may sit closer to Together Money, United Trust Bank or Spring Finance.

Other files need a different lender flavour. A broker may look at Optimum Credit for second-charge borrowing, Paragon Bank secured lending, Norton Finance broker-led cases, Masthaven-style specialist finance, or even an older 1st Stop homeowner-loan route. If the borrower already banks elsewhere, they may also compare a TSB secured loan enquiry with those broker-only choices.

Remortgaging later

A secured loan can affect remortgaging because it sits behind the main mortgage as another charge. Some people keep the loan separate. Others remortgage later and repay it if the figures allow. The new lender will consider equity, affordability, and the secured loan balance, so it is worth thinking beyond the first monthly payment.

When the borrower is comparing second-charge lending with a remortgage, the current mortgage rate and any early repayment charge are important. If the existing mortgage is cheap or tied in, a secured loan can be less disruptive. If the current mortgage is already on a high variable rate, remortgaging may be worth a proper look.

Repaying the loan without getting boxed in

The safest way to manage a secured loan is to keep the repayment boring. Direct debit, enough headroom in the bank account, and early contact with the lender if money gets tight. Overpayments can help reduce interest, but the terms need to be checked first because some products have early repayment charges.

A secured loan can be useful when the reason is clear and the repayment plan is realistic. It can be a poor fit when borrowing is only patching short-term spending, or when the term is stretched just to make the monthly payment look comfortable.

Purpose of a secured loan FAQs

What is a secured loan?

A secured loan is borrowing tied to an asset, usually a home. If the borrower does not keep up the repayments, that asset can be at risk.

What can a secured loan be used for?

Common uses include home improvements, debt consolidation, large purchases, business plans and property-related costs. The lender may still ask what the money is for.

Can a secured loan help with poor credit?

It can help some borrowers access finance where unsecured lenders say no, but poor credit usually affects the rate, lender choice and checks required.

Will a secured loan affect a remortgage?

Yes, it can. The loan reduces available equity and the repayment is included in the affordability assessment. It does not always stop a remortgage, but it can narrow the options.