Best Secured 10 Year Loans – Fixed Low Rates 2026

A 10-year secured loan can work well when you need a larger amount and want a fixed, manageable repayment period. The loan is usually secured against your home, so the lender looks at your equity, income, credit history and existing mortgage before making a decision.

The right deal is not always the lowest headline rate. It depends on the total cost, fees, loan-to-value ratio, repayment flexibility, and whether the lender is comfortable with your circumstances. Comparing the secured loan rates available to you is usually more useful than chasing a rate you may not qualify for.

Access to a broad specialist lender panel with 100’s of secured loan products & high rates of acceptance!

- Our secured loan brokers match the term of the loan to remaining term of your mortgage

- Great for clearing other loans/credit cards/existing car credit

- New lenders for 2026 now available

- High loan-to-value (LTV) with many lenders

- Same day decisions. Quick & simple

- Keep your existing mortgage with no hassles

- Soft footprint credit search that won’t affect your credit rating

- We Offer Homeowner Loans From The UK’s Top Lenders . Flexible Repayments. Exclusive Rates – Secured Loan Brokers

- Rates from just 4.47%

- Borrow up to 100% of the value of your home ( subject to status)

- No obligation to proceed

- We have broker only lenders that are not featured on the far from impartial comparison engine sites.

Decision-in-principle application

How a 10-year secured loan works

A secured loan uses an asset, usually your property, as security. This makes it different from an unsecured loan, which is why a lender may consider higher borrowing limits, longer repayment terms, or a case with imperfect credit. If the loan sits behind your main mortgage, it is usually treated as a second-charge mortgage.

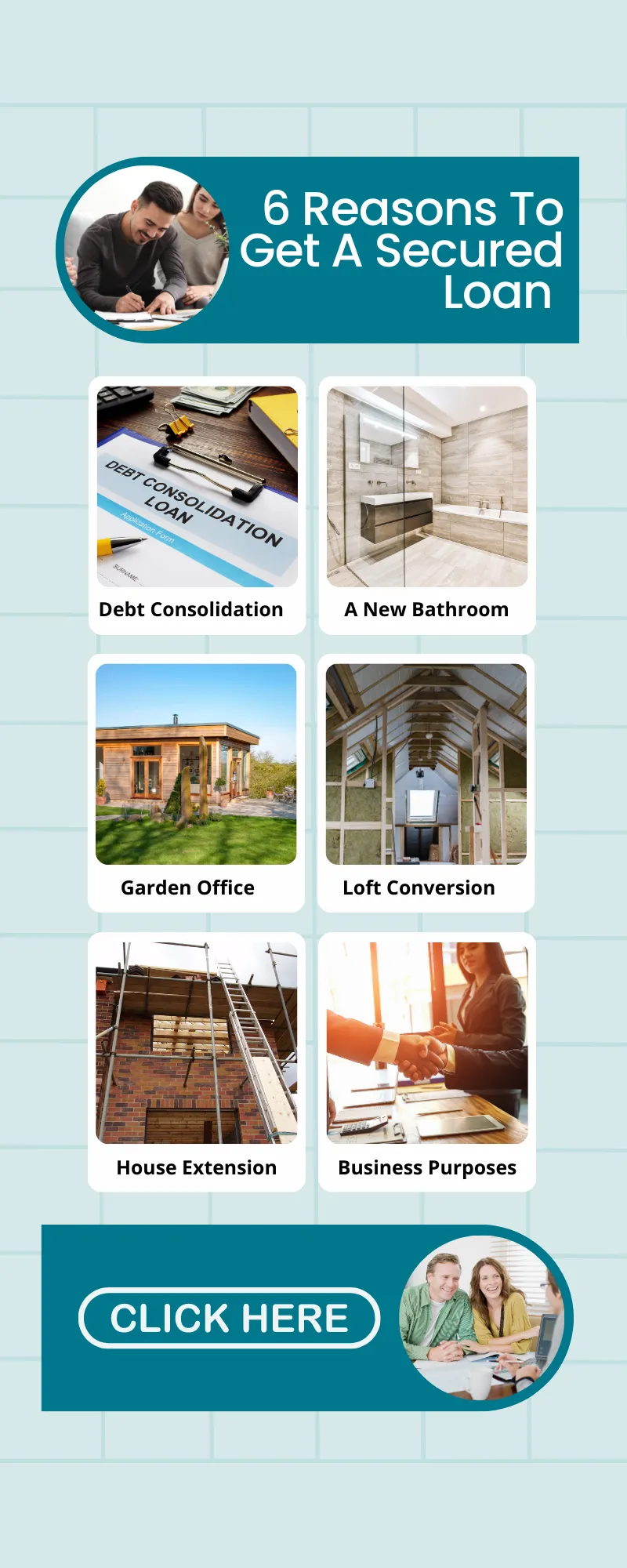

Ten years is long enough to spread the repayments, but not so long that the borrowing runs on for decades. It can suit planned spending, such as work on a property, or a controlled debt consolidation loan, where the aim is to replace several expensive payments with a single monthly commitment.

The practical question is not just whether a lender will say yes. It is whether the payment still leaves enough room for normal bills, insurance, repairs and the odd expensive month. A secured loan should solve a problem, not leave the household needing fresh credit a few months later.

Benefits and drawbacks

The main benefit is that you may be able to borrow more than with a personal loan, particularly if you have useful equity in your home. Some borrowers also prefer the certainty of a fixed-rate secured loan, especially when budgeting over several years.

The drawback is simple: your home can be at risk if you do not keep up the repayments. Longer terms can also mean paying more interest overall, even where the monthly payment looks comfortable. A 10-year term should be chosen because it fits your budget, not just because it reduces the monthly figure.

It is also worth asking how the loan behaves if you repay early, move house or want to remortgage later. Some products are flexible, while others look attractive at the start but become expensive if your plans change. That is where the small print matters.

Each of these loan types uses a specific asset as collateral and has its unique features and benefits.

Home equity, second charges and lender choice

Home equity loans and second mortgages both use property value to support the borrowing. The difference in outcome often comes down to the lender’s credit appetite, fees and how they treat income, arrears, defaults or self-employment.

For example, one borrower may be better placed with 1st Stop, Blemain Finance, Masthaven Bank, Norton Finance or United Trust Bank. Another may fit Pepper Money, Precise, Together Money, Paragon Bank, Spring Finance or Optimum Credit, depending on the case.

That does not mean one lender is universally better than another. A lender that is excellent for a clean, low-risk case may be a poor fit for recent arrears, complex income or a high loan-to-value application. The matching matters more than the name on the offer.

When a 10-year term may suit the job

Borrowers often use this type of lending for substantial home work, essential repairs or clearing expensive credit. A £25,000 loan can be enough for a focused project, while larger schemes may need a different structure. For property improvements, it can also be worth comparing specialist secured borrowing with Nationwide home improvement loans, NatWest home improvement options or Santander home improvement loans.

Second mortgages can be beneficial for financing larger expenses such as home improvements, paying for college tuition, or consolidating debt.

Some homeowners apply alone, but a joint secured loan can make sense where both applicants have income and share the mortgage. If you prefer to keep things online, a secured loan with no phone calls may be worth considering, provided the case is straightforward enough for that route.

For home improvements, the lender may want to understand the scale of the work and whether it improves the property. For debt consolidation, the question is whether the old debts will actually be cleared and whether the new payment is sustainable over the full term.

Eligibility, credit and affordability

Eligibility depends on equity, income, property type, existing mortgage balance, credit history and the purpose of the loan. Lenders may consider employed income, self-employed earnings, pensions or other regular sources, but they still need to be satisfied that the repayments are affordable.

Other criteria may include a minimum credit score, evidence of income, and a positive credit history. The specifics can vary among lenders, but these are the most common requirements.

A weaker credit file does not always mean a decline. There are homeowner loans for bad credit and broader secured loans with bad credit, but they still need to pass affordability and property checks. Defaults, arrears and CCJs matter, but different lenders treat them differently.

Costs to check before you apply

Alongside the rate, check valuation fees, broker fees, lender fees, early repayment charges and the total amount repayable. A low payment can still be expensive if the term is stretched too far. For some people, second mortgage rates are attractive; for others, the better answer may be to borrow less, choose a shorter term or delay until the credit file improves.

TSB secured loans, and some high-street options may suit cleaner credit profiles, while specialist lenders can be more flexible but may cost more. The intended use of the secured loan can also affect which lender is suitable.

Ask for the payment, the full amount repayable and any exit costs in plain numbers. If a quote only feels affordable because the term is stretched, it is worth pausing. A slightly higher monthly payment over a shorter term may save money, but only if it leaves enough room in the budget.

Alternatives to a 10-year secured loan

A 10-year secured loan is not the only answer. Smaller borrowing may be better handled by an unsecured personal loan, savings, a shorter-term facility or, in some cases, a remortgage. The right option depends on the amount, urgency, rate, fees and risk to the home.

Personal loans are often unsecured, meaning they don’t require collateral. A personal loan can be used for various purposes, from consolidating debts to funding home improvements.

Before applying, it is worth setting out what the money is for, what payment would still feel comfortable in a bad month, and whether the loan improves your position rather than just moving the problem. The safest secured loan is usually the one that fits the household budget, not the one with the boldest advert.