Best Mortgages For Over 50s In 2026

1st UK has some superior mortgages for the over 50s

How can the over-50s secure such low-rate finance?

There are two reasons for this:

- Primarily, a pension company or the government is unlikely to default on a pension responsibility.

- Secondly, lending institutions consider the UK property sector stable. Furthermore, an individual’s home offers sound collateral.

Therefore, lending to those in their 50’s and above can be seen as low risk. This is now an excellent time to consider 1st UK Mortgages’s panel of mortgages for over-50s.

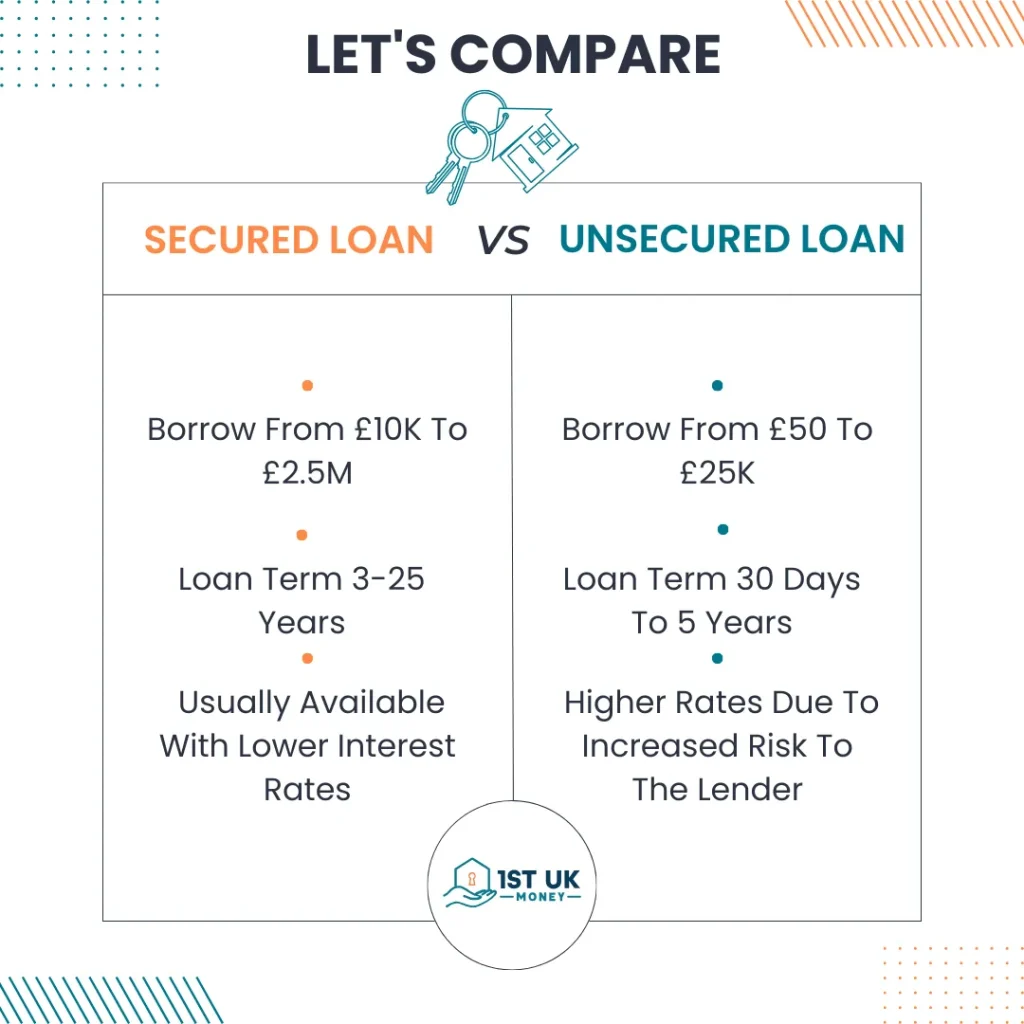

What if I don’t want to make a monthly payment or can’t make one?

Desirable deals are available if you’re seeking to access money tied up in your property.

Mortgages For Over 50s Or 55? | Expert Advice From Specialists

- FCA Approved Advisors. Get A Decision Today.

- Poor Credit, Sub Prime, Default, IVA, CCJ OK

- Get Your Quotes From Our Expert Providers

- Low Interest Rates. 2 Year Fixed, 3 YeaFixed, 5 Year Fixed, Tracker.

We Search The Entire Market Saving You Time & Money On Your Over 50s Mortgage

Over Fifties Pre-Decision In Principle Application Form:

Don’t miss out on some of the best over-50 mortgage rates in the UK

Our bespoke mortgage quotation service is fast, secure, and convenient. Fill in our easy-to-use forms for an up-to-date view of the current market – with no obligation to proceed.

Rest assured that your data will not be shared with any third parties, so there’s no risk in discovering what you could save today. With excellent rates available right now, you won’t want to delay getting your quote.

For Those Over The Age Of 50, Securing A Mortgage Can Often Be Difficult.

The mortgage and financing industry has not kept pace with the advancements made in the medical field. People are generally healthier, live longer, and work well past the traditional retirement age, which means they earn more over their lifetimes.

Although securing a mortgage over the age of 50 is possible, finding a deal that fits both your lifestyle and your budget can sometimes be complex.

How can I increase my chances of securing a mortgage over the age of 50?

Getting a mortgage over 50 in the UK can sometimes be a challenge – especially if you’ve had some credit issues in the past. However, you can take steps to increase your chances of being approved for a mortgage regardless of your age.

First and foremost, it is important to begin by obtaining a copy of your current credit report and score from one of the UK’s main credit reference agencies such as Experian.

This will allow you to review any errors in the report and identify opportunities for improvement. Once complete, make sure to check these reports regularly to stay up to date on any changes that may occur.

In addition, specific lenders specialise in providing mortgages for those aged over 50 or retired. Some even offer higher loan-to-value ratios than traditional lenders, which can further improve your chances of approval should you qualify for them (always consult a professional financial advisor before taking out any loan agreement).

How Mortgages for Over 50s Can Help Repay Your Existing Mortgage

Furthermore, researching options suitable for those over 50 can often lead to better rates than those offered by other lenders, so look into this at length before applying.

Another key factor influencing approval is proof of regular income or pension payments, as documented through bank statements or pay slips.

Most traditional providers will require this before acceptance, so make sure these documents are readily available, along with whatever information they need regarding your assets and liabilities, should they be deemed relevant during the assessment.

Finally, always consider discussing your requirements directly with potential lenders, whether online, by telephone, or in person at their local branch office.

Most banks have dedicated teams that focus specifically on applications from customers over 50, who may require special consideration due to lower incomes or other factors that affect suitability.

So do take advantage of their expertise whenever possible.

If you follow all these steps correctly, you can significantly increase your chances of being approved for mortgages over 50 in the UK.

What Mortgage Companies Consider For Applicants Over 50

Medical information suggesting that people are living longer and earning more has prompted many mortgage companies to begin catering to this specific market.

There is potential for companies to earn more by working with individuals over 50, and there are several reasons why someone in this age group may want to secure a mortgage.

For some, it may be their first opportunity to own a home, or perhaps they want to refinance their current mortgage. For whatever reason, mortgage companies ask applicants, “Why now?”

While knowing why the applicant is interested in a mortgage is essential, brokers must also see whether they can afford it.

Applicants still in the workforce must provide proof of their annual income so the broker can determine if they qualify for a mortgage.

On the other hand, if the applicant is retired, he or she will have to provide documentation demonstrating that he or she has the funding needed to make monthly payments in the form of savings, investments, or pension payments.

Even though individuals are living longer, mortgage brokers need to determine whether applicants will live long enough to repay the amount owed.

Many mortgage companies have a maximum age limit for accepting new mortgages for those over 50.

If the applicant is a good candidate for a mortgage but may not be able to repay the full amount due to age, a broker may ask them to appoint someone to be responsible for payments after their death.

What Mortgage Options Are Available For Those Over 50

There are many types of mortgages available, so it is essential for individuals to consider what they need and want in a mortgage before comparing offers.

Applicants should ask themselves some critical questions when choosing a mortgage: what loan-to-value ratio are they comfortable with for their current property, how much funding are they looking for, and what initial interest rate best fits their current budget?

Answering these questions will help narrow down the many mortgage options available.

In addition to these questions, applicants should consider what monthly payments they are comfortable with. There are two payment options: fixed–rate or variable–rate. Fixed-rate payments remain the same every month and are easier to incorporate into an existing budget.

Variable rate payments vary from one month to the next, depending on the current interest rates – sometimes, this works in the applicant’s favour, and sometimes it causes payments to be very high.

If you’ve ended up with some bad credit, those over 50 can still consider bad credit remortgages from 1st UK, as loans from pensions and investments are seen by lenders as a good, stable income.

Comparing Mortgage For Over 50 Offers

Once the mortgage needs and wants have been determined, it is essential that applicants compare multiple mortgage options from various lenders.

No two mortgage company are the same, and the offers these companies can make to applicants will vary immensely, even if the overall structure of the mortgage is the same.

The key aspects to consider when making a final decision are the duration of the terms, fixed rate or variable rate payment, and if the mortgage meets your needs.

There are some great offers for the over 50s, over 60s and over 65s, too, in 2026.

Best Mortgages For Over 50s FAQs

Can I get a 25-year mortgage if I’m 50?

Yes, you can. In the UK, there is no maximum age for taking out a mortgage. However, lenders will consider your age and whether you are likely to remain employed and able to make mortgage repayments 25 years down the line.

If you are 50 or over and want to take out a 25-year mortgage, shopping around and comparing products from various lenders is essential. A good credit rating is also crucial, as it helps you secure the best interest rate on your mortgage.

Can I get a mortgage at 55 years old?

You may be able to get a mortgage at 55 years old and live in the UK, but it will depend on many factors, including your income, credit score, and current debt levels.

You may want to speak with a mortgage broker or bank to learn more about your options. Some lenders offer mortgages to people over the age of 55. Keep in mind that you may have to pay a slightly higher interest rate if you are over the age of 55.

What is the difference between an interest-only mortgage and a repayment mortgage?

With an interest-only mortgage, you only pay the interest on the loan each month. You don’t make any payments toward the loan principal.

This type of mortgage is best for people who know they won’t be in their home for long periods or who plan to invest the money they would have used for a down payment in other assets that offer a higher return.

A repayment mortgage is different in that you not only pay the interest each month, but you also make payments towards the principal amount of the loan.

This type of mortgage is best suited for people who plan to stay in their home for a long time and want to see their equity grow.