Best Equity Release Companies – Top Providers List For 2026

Finding the right equity release provider depends on your age, property value, borrowing needs, repayment preferences and the protections built into the plan. The best providers are usually those that offer clear fees, fixed or capped rates, flexible repayments and proper safeguards for your home and estate.

Equity release can provide tax-free money as a lump sum, smaller drawdowns or a mixture of both. Before choosing a plan, compare the cost, lender criteria, early repayment charges, advice process and whether the provider is a member of the Equity Release Council.

Low Rate Equity Release Plans For 2026 – Free Valuation

- Remove tax-free cash from your home with age flexibility

- 4.37% APR for equity release with our selected provider

- Zero lender fees and hidden extras

- Free property valuation

- No product fees with our equity release companies

- Choice to get a mortgage to purchase another home

- Make a monthly payment if you so choose

- Help out a member of your family in buying their own home with a small mortgage

- Retain 100% ownership of your home while continuing to live there

How much money can you release from your property?

The amount you can release is usually based on your age, property value, health, plan type and loan-to-value limit. As a simple example, 65% of a £340,000 valuation would be £221,000, although many mainstream plans offer lower maximum percentages.

Looking For The Best Equity Release Companies? Release Tax-Free Cash. Get Your Quote Below

Main points to compare before borrowing in retirement:

- Check the interest rate, whether it is fixed or capped, and how interest builds up over time.

- Compare advice fees, valuation fees, legal fees, product fees and any early repayment charges.

- Look for voluntary repayment options if you want to reduce the final loan balance.

- Consider the effect on means-tested benefits, inheritance plans and future downsizing.

- Review the loan-to-value offered, as higher borrowing normally increases the long-term cost.

- Use the monthly equivalent rate and overall cost illustrations to compare like-for-like.

What You Need to Look for in an Equity Release Provider

A suitable provider should be regulated by the Financial Conduct Authority, use a qualified adviser and explain the full cost before you proceed. Equity Release Council membership is also important because it normally includes protections such as the right to remain in your home and a no-negative-equity guarantee.

- Choose providers that are members of, or aligned with, the standards of the Equity Release Council.

- Check whether the plan allows fixed or capped rates, inheritance protection and future drawdown.

- Look for clear information on early repayment charges, voluntary repayments and administration fees.

- Make sure the property rules fit your home, especially if it is leasehold, ex-council, non-standard construction or in a higher-risk flood area.

- Review customer feedback, but base the final decision on suitability, affordability and written illustrations.

If you are aged 55 or over, equity release may help you clear borrowing, improve your home, support family or add retirement income. Some plans also let you protect a percentage of the property value for inheritance.

Benefits Of Our Services:

- Release equity from your home as a cash sum or via regular payments

- Exclusive rates and offerings from the top equity release providers

- Release money for repairs or home improvements like a new kitchen or bathroom.

- Help a family member purchase their first home.

- Pay off all your credit cards and loans and have zero monthly payments.

- Switch to a better lifestyle, change your car or have a well-deserved holiday.

- 100% independent, securing you quotes from the UK’s leading equity release companies.

Types of Equity Release Schemes: Lifetime Mortgages and Home Reversion Plans

A lifetime mortgage is the most common UK equity release product. It is secured against your home, which remains yours, and the loan is usually repaid when you die or move into long-term care. A home reversion plan works differently: you sell part or all of the property in exchange for money while retaining the right to live there.

Here’s an overview of the two Equity Release types:

| Equity Release Scheme | Product Features | Suitable For |

|---|---|---|

| Lifetime Mortgage | No need to move out. Interest rolls up over time. There is an option to ring-fence inheritance. Varied interest rates can be fixed or capped. | Those looking to utilise the property value while living in their home. |

| Home Reversion Plan | Sell part or all your property in exchange for a lump sum or regular income, and live rent-free. | Those preferring certainty of funds over property ownership. |

A List Of Equity Release Providers (UK)

The providers below include major later-life lenders, insurers and home reversion administrators. Criteria change, so a broker or adviser should confirm availability, rates and eligibility before you apply.

Just Retirement

Just Retirement offers drawdown and lump-sum lifetime mortgage options, generally from age 60. The minimum release is commonly £10,000, with property and location rules applying, including Northern Ireland on selected plans.

Retirement Plus

Retirement Plus is linked with home reversion administration rather than mainstream lifetime mortgages. It is approved by the Equity Release Council, and customers interested in home reversion should compare it with those offered by specialist administrators such as Retirement Bridge Group.

Pure Retirement best equity release interest rates

Pure Retirement focuses entirely on equity release and offers lifetime mortgage options for homeowners aged 55 or over. Drawdown can be useful when you do not need the full amount immediately, as interest is normally charged only on the amount released.

Hodge Lifetime’s lowest equity release rates

Hodge Lifetime specialises in retirement finance and offers lifetime mortgage products with a no-negative-equity guarantee. Typical criteria include age limits, property valuation rules, standard construction requirements, and lease-length conditions.

Aviva’s best equity release deal

Aviva provides two equity release products: a lump-sum option and a flexible drawdown plan for homeowners aged 55 or over. Aviva does consider equity release on leasehold properties, subject to lease length and property criteria, and may allow voluntary annual repayments.

Retirement Bridge Group best drawdown equity release

Retirement Bridge Group is a major administrator of home reversion plans, including Bridgewater-style rent-free, fixed-rent and escalating-rent options. These plans suit customers who want certainty of funds but are comfortable selling a share of their home.

Nationwide Building Society’s best equity release schemes

Nationwide has offered later-life lending options with criteria based on age, property value, and loan-to-value ratio. The important points to compare are early repayment charges, downsizing protection, and whether the product is a lifetime mortgage, a RIO mortgage, or another later-life product.

LV= Liverpool Victoria best equity release rates UK

LV= offers lifetime mortgage options for homeowners who meet its age, property value and loan size rules. The LV= equity release plan may include lump-sum or drawdown options, with future withdrawals subject to minimum transaction rules.

Overview Of Equity Release Interest Rates 2026

| Aspect | Detail |

|---|---|

| Lowest Interest Rate | 4.37% (AER) fixed for life |

| Highest Interest Rate | 8.98% (AER) |

| Average Interest Rate | 5.21% (From Market Report by the Equity Release Council) |

| General Rule | 5% excellent, 6% average, 7%+ for substantial borrowing with more product features |

| Factors Affecting Rates | Loan to Value, Credit History, Product Features, Lending Criteria, Age, Marital Status |

| AER vs MER | AER (Annual Equivalent Rate), MER (Monthly Equivalent Rate) |

| Fixed vs Variable Rates | The majority are fixed; variable rates are typically linked to the Consumer Price Index (CPI) |

| Interest Rate Trends | Lifetime mortgage interest rates are at an all-time low; lower rates have continued to fall |

Legal and General Home Finance has flexible repayment options and great customer feedback

Legal and General Home Finance is a large provider in the equity release market. With L & G equity release, customers may choose lump-sum or drawdown options, subject to age, property value, health and product criteria.

One Family Lifetime Mortgages LTD financial solutions

OneFamily offers lifetime mortgages including interest roll-up, voluntary repayment and interest-payment options. The right choice depends on whether you want no monthly payments, partial repayments or regular interest payments to limit roll-up.

More2Life with the best equity release process

More2Life provides lifetime mortgage ranges including Capital Choice, Maximum Choice, Tailored Choice and Flexi Choice. Some products allow larger releases, some allow higher voluntary repayments, and some are designed around health or drawdown needs.

Costs And Repayment Of The Top Equity Release Companies

| Aspect | Details |

|---|---|

| Cost Components | Includes advice fees, repayment fees, application fees, and tax considerations. |

| Advice Fees | Essential for the process can be a fixed amount or a percentage of the released amount. |

| Repayment Fees | Consider potential early repayment charges. |

| Tax Implications | There is no tax on released equity, but implications for how the money is used (e.g., Inheritance Tax). |

| Application Fees | This may include valuation, solicitor’s, and lender’s fees. |

| Repayment Options | Interest can be repaid in full or partially, monthly or in lump sums, without penalty. |

| Equity Release Suitability | Advisers help compare options and ensure the plan suits individual needs. |

Canada Life – one of the top equity release providers

Canada Life offers lifetime mortgages with lump-sum, drawdown and repayment-style features. Lifetime mortgages from Canada Life can include inheritance protection, further borrowing and a cash reserve, while selected plans may suit second homes. Its plans also include a no negative equity guarantee.

Standard Life/Age Partnership Calculator Equity Release

Standard Life has used referral and partnership arrangements rather than directly offering every product itself. A whole-of-market adviser can compare the best UK equity release providers and provide a Key Facts Illustration before you proceed.

Which UK Equity Release Companies Are Members Of The Equity Release Council?

Several lenders and advisers are members of the Equity Release Council or work to its standards. Membership is useful because it gives customers a clearer framework for advice, product safeguards and complaints.

The complete list is as follows, including the top 10 equity release companies:

- Just Mortgages and the Just Group, with a qualified equity release adviser, offer greater flexibility

- LV= for an excellent initial lump sum

- OneFamily Lifetime Mortgages is one of the leading equity release providers

- Santander mortgages for over 70’s that offer two lifetime mortgages and other tailored solutions

- More2Life is one of the flexible equity release lenders

- Pure Retirement equity release brokers with a money-back guarantee

- Responsible Lending for the later-life mortgage market and greater flexibility

- Crown Equity Release is working with a qualified equity release adviser

- Aviva equity release services with excellent customer service and compound interest

- Legal & General Home Finance – one of the top equity release providers

- Canada Life lifetime mortgage lender, offering home finance to repay existing debts

- Retirement Bridge Group has various equity release mortgages and retirement services

- Nationwide Building Society – one of the top equity release companies

- Standard Life Home Finance for Later Life Borrowers with no monthly income

- Scottish Widows for the best equity release journey with flexible repayment options

- Hodge Bank with low early repayment charges and with a reasonable lump sum upfront

- Key Retirement to find the best equity release provider for people with financial goals

Know your options for the best company for equity release

The Lifetime Mortgage

A lifetime mortgage stays secured on your main home for the rest of your life unless you repay it earlier or move into long-term care. You may be able to ring-fence inheritance, make voluntary payments or let interest roll up until the property is sold.

Best Equity Release Companies UK for 2026

The best company is not simply the one with the lowest rate. The better choice is the provider that fits your property, borrowing amount, repayment plans, inheritance goals and need for future flexibility.

Things to know about Lifetime Mortgages:

- The usual minimum age is 55, although some providers set a higher age.

- Maximum borrowing depends on age, property value, health and product features.

- Interest should be fixed or capped, and reputable providers include a no-negative-equity guarantee.

- You can usually move home if the new property meets the lender’s security rules.

- Taking smaller drawdowns can cost less than taking one large lump sum at the start.

More detailed equity release guides for the top equity release companies in the UK:

- Pros and Cons of various equity release plans with interest payments

- For 90 Years And Above for releasing equity near the end of life

- Equity Release For Under 55 with two equity release options and equity release interest payments

The Best Equity Release Providers List Plus Questions And Answers

These shorter answers keep the useful internal resources without repeating the same provider claims. Start with whether you should consider equity release, then compare products with advice.

- Lloyds, care fees and later-life borrowing: see care home fees.

- RBS and family support: see gift money to the family and the Royal Bank of Scotland equity release guide.

- Santander and older borrowers: see over 70s.

- HSBC and education costs: see HSBC equity release and using equity release for school fees.

- Saga and later retirement: see Saga equity release reviews, people over 80 and pensioners.

- Sunlife and moving plans: see Sunlife lifetime mortgages, using equity release to buy another property, and over 55 equity release.

- Nationwide: see Nationwide offers three types of equity release products.

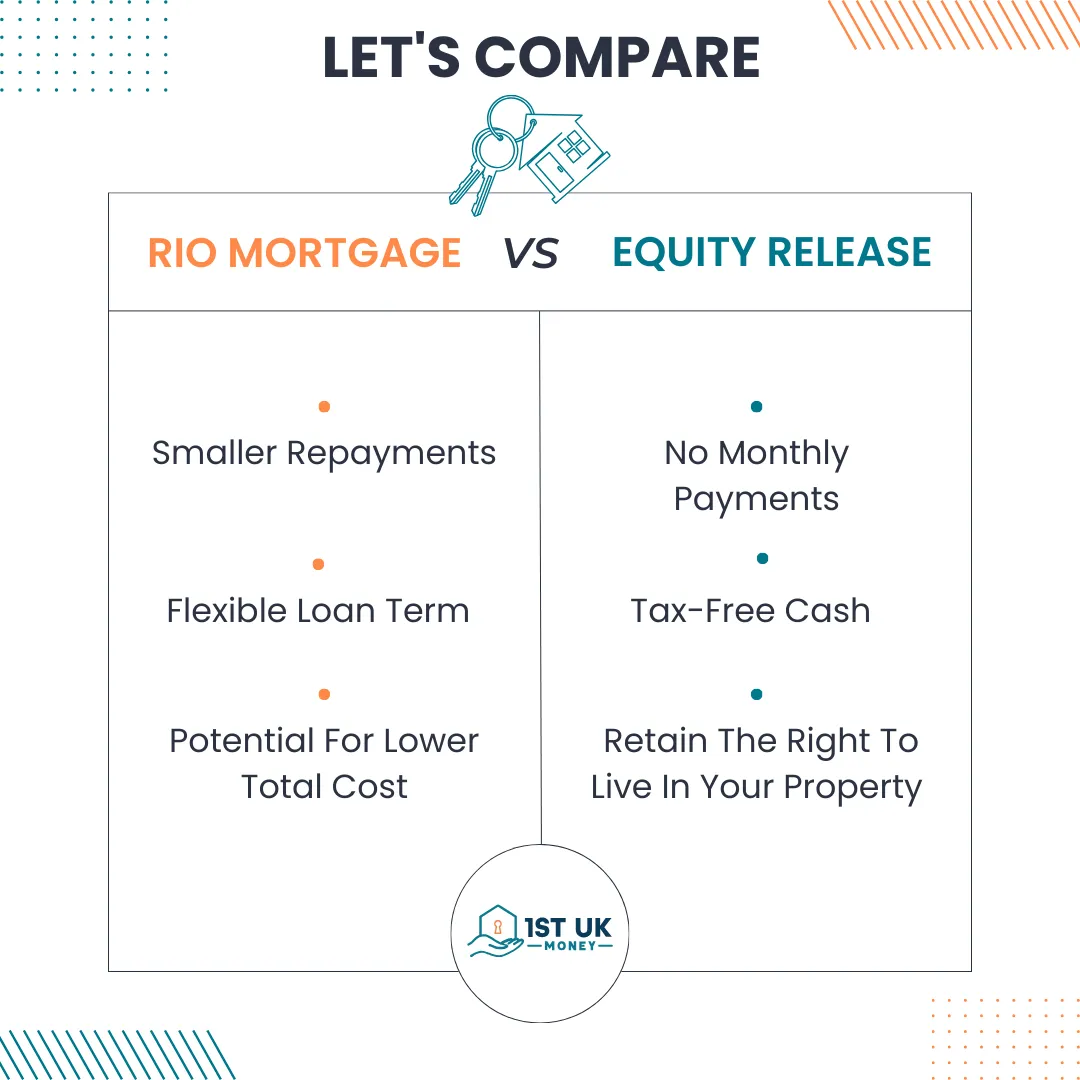

- Leeds Building Society: Leeds Building Society does not offer equity release plans but has RIO mortgages as an alternative.

What Are The Latest And Best Equity Release Rates In The UK?

Rates vary by lender, loan-to-value ratio, age, health, repayment features, and product type. Use the table above as a comparison guide, but request a current illustration before making a decision because available rates and criteria can change.

For homeowners aged 60+, the most suitable plan may be a lifetime mortgage, a RIO mortgage or another later-life lending product, depending on income, affordability and future plans.