Best Secured Loan Broker Cheapest Rates Guaranteed For 2026

Access to a broad specialist lender panel with hundreds of secured loan products

- Match the loan term to the remaining term of your mortgage

- Useful for clearing loans, credit cards or existing car finance

- New lender options for 2026 now available

- High loan-to-value options with some lenders

- Same-day decisions where the case is straightforward

- Keep your existing mortgage in place where suitable

- Soft footprint credit search that will not affect your credit rating

- Homeowner loans from major and specialist UK lenders

- Rates from 7.49%, subject to status and lender criteria

- Borrow up to 100% of the value of your home, subject to status

- No obligation to proceed

- Access to lenders that do not usually appear on comparison sites

Pre-decision application form for prime, light adverse and heavy adverse credit cases

Credit problems do not always rule out a secured loan

Since the cost-of-living squeeze began, more homeowners have looked at secured borrowing, especially where a standard bank loan has been declined. A homeowner loan with bad credit case is not always simple, but using your home as security can open up lenders that would not consider an unsecured application. It may also help you compare the best secured loan rates available for your circumstances.

Borrowers sometimes try to deal with lenders themselves. That can work if your income, credit file and property are all straightforward. It becomes harder when there are missed payments, unusual income, a high loan-to-value request, an old CCJ, a Debt Management Plan or a property issue that could affect valuation.

An execution-only route also puts more work on you. You need to know the product type, the fees, the interest rate, the property details, the lender’s income rules, and whether the loan is likely to pass affordability checks. One small mismatch can cause a decline and, in some cases, leave a hard search on your credit file.

- Know whether a second-charge mortgage is suitable before you apply.

- Check how the lender treats leasehold property, valuation issues and existing mortgage balances.

- Understand which types of income count for affordability.

- Compare fees, rate type, early repayment terms and the total amount repayable.

Direct lender or brokered secured loan?

Most people are really choosing between a direct lender and a brokered route. Direct lenders deal with you themselves. A broker compares lenders and routes the case to the one where it has the best chance of passing. That matters with secured loans with bad credit, because lenders’ criteria can differ significantly, even when two products look similar on the surface.

The direct route means comparing interest rates, application fees, completion fees, valuation charges and the long-term cost yourself. A low rate is not always the cheapest answer if the fees are high or the lender is unlikely to accept the case.

The broker route usually involves more questions at the start: income, outgoings, employment, benefit income, pension income, existing credit, mortgage conduct and property details. It can feel a little more involved, but that detail is what prevents a weak application from being sent to the wrong lender.

Why lender criteria matter

Specialist secured-loan brokers often know which lenders are comfortable with different levels of risk. One lender may consider a recent CCJ, while another may only accept one that is over a year old. A Debt Management Plan might be fine with one lender if it has been maintained cleanly, but not with another if there has been a missed payment or a recent default.

This is where the real work happens. The rate is only part of the deal. The best application is the one that meets the lender’s rules before submission.

Where a broker can add value

A high-street lender can only discuss its own products. That may be enough for a clean case, but it is limiting if you need to compare several lenders. A secured-loan broker should consider the total cost, not just the rate, and explain why a particular lender is being recommended.

Speed is another reason people use brokers. A good broker will chase lenders, check documents early, speak to underwriters where needed and keep the application moving. That practical work is not glamorous, but it often makes the difference between a case drifting and a case completing.

Many lenders also use intermediary channels because brokers do much of the sorting before a case reaches the lender. Customers have long chosen to use a secured loan broker for that extra filtering and explanation.

What a broker should do

- Explain which income types different lenders will accept.

- Compare suitable secured loan products and the full cost of each one.

- Assess whether the loan amount, term and monthly payment are realistic.

- Route the application to a lender that is likely to accept the credit profile.

- Look at broker-only or intermediary-only products where they are relevant.

Many lenders now use broker channels for specialist secured loans. Some products are not shown on comparison sites because the lender wants the case checked properly before it reaches underwriting.

When a broker may be worth using

A broker is often useful when the case is not neat: adverse credit, fluctuating income, high borrowing, a need to consolidate several debts, or an existing mortgage deal that you do not want to disturb. A good broker will still ask direct questions, because a lender cannot give a proper answer without the full picture.

No one can honestly say there is one best secured loan for every UK borrower. The cheapest rates are usually reserved for people with strong credit, low borrowing relative to the property’s value, and a clean mortgage history. Other borrowers may still get a sensible result, but the lender and rate will be different.

Do you need a broker?

Some borrowers search for no-broker-fee loans because they do not want fees added to the balance. That is understandable. The issue is that some lenders are broker-only, and a declined direct application can be more costly than getting the case placed correctly from the start.

The right broker should explain any fee, show the total amount payable and make clear why the recommended lender is suitable. If the broker cannot explain that in plain English, keep asking until the numbers make sense.

The best secured loan is not simply the lowest advertised rate. It is the lowest suitable cost from a lender that is willing to accept your income, credit file, property and loan-to-value position.

Check the real cost, not just the rate

A secured loan can look cheap on the monthly payment, especially if the term is long. That does not always mean it is cheap overall. A loan spread over twenty or twenty-five years may reduce pressure on the household budget, but it can also mean paying interest for much longer. This is particularly important when using a secured loan to clear credit cards, store cards or car finance that would otherwise have ended sooner.

Ask for the monthly payment, the total amount repayable, any lender fee, any broker fee, the valuation cost, whether the rate is fixed or variable and whether early repayment charges apply. It is also worth asking what happens if you remortgage later, move home, make overpayments or want to clear the balance early. The answer can change which loan is actually the better deal.

If the purpose is debt consolidation, take care not to pay off short-term debts only to build them back up again. The new payment should leave enough breathing space without encouraging another round of borrowing. That is not a sales point; it is just the part people may regret later if it is not discussed properly at the start.

Secured loan terms worth knowing

| Term | Description |

|---|---|

| Second Charge Mortgages | A loan secured against your home in addition to your existing mortgage. |

| Debt Management Plan (DMP) | A repayment arrangement with creditors. Some lenders may consider applicants in a well-maintained DMP. |

| County Court Judgments (CCJs) | A court record showing unpaid debt. Lenders treat CCJs differently depending on age, value and whether they are satisfied. |

| Loan-to-Value (LTV) | The loan amount compared with the value of the property used as security. |

Examples of lender differences

| Provider | LTV Range | Interest Rate Options | Notes |

|---|---|---|---|

| Pepper Money | Up to 100% | Fixed, Variable | May suit some self-employed or non-standard cases. |

| United Trust Bank | High | Fixed, Tracker | Usually wants a mortgage history and clear affordability. |

| Norton Home Loans | Varies | Fixed, Variable | Can be useful where smaller loans or specialist criteria are needed. |

| West One | Up to 85% | Fixed, Variable | Often considered for larger or more specialist borrowing. |

Risks to check before applying

| Risk Factor | Description | What to check |

|---|---|---|

| Home Repossession | Your home may be at risk if repayments are not made. | Use a repayment that still works if bills rise. |

| Interest Rates | Rates vary by credit profile, LTV and term. | Compare the total cost, not just the headline rate. |

| Loan Terms | A longer term can reduce monthly payments but increase total interest. | Choose the shortest term that remains affordable. |

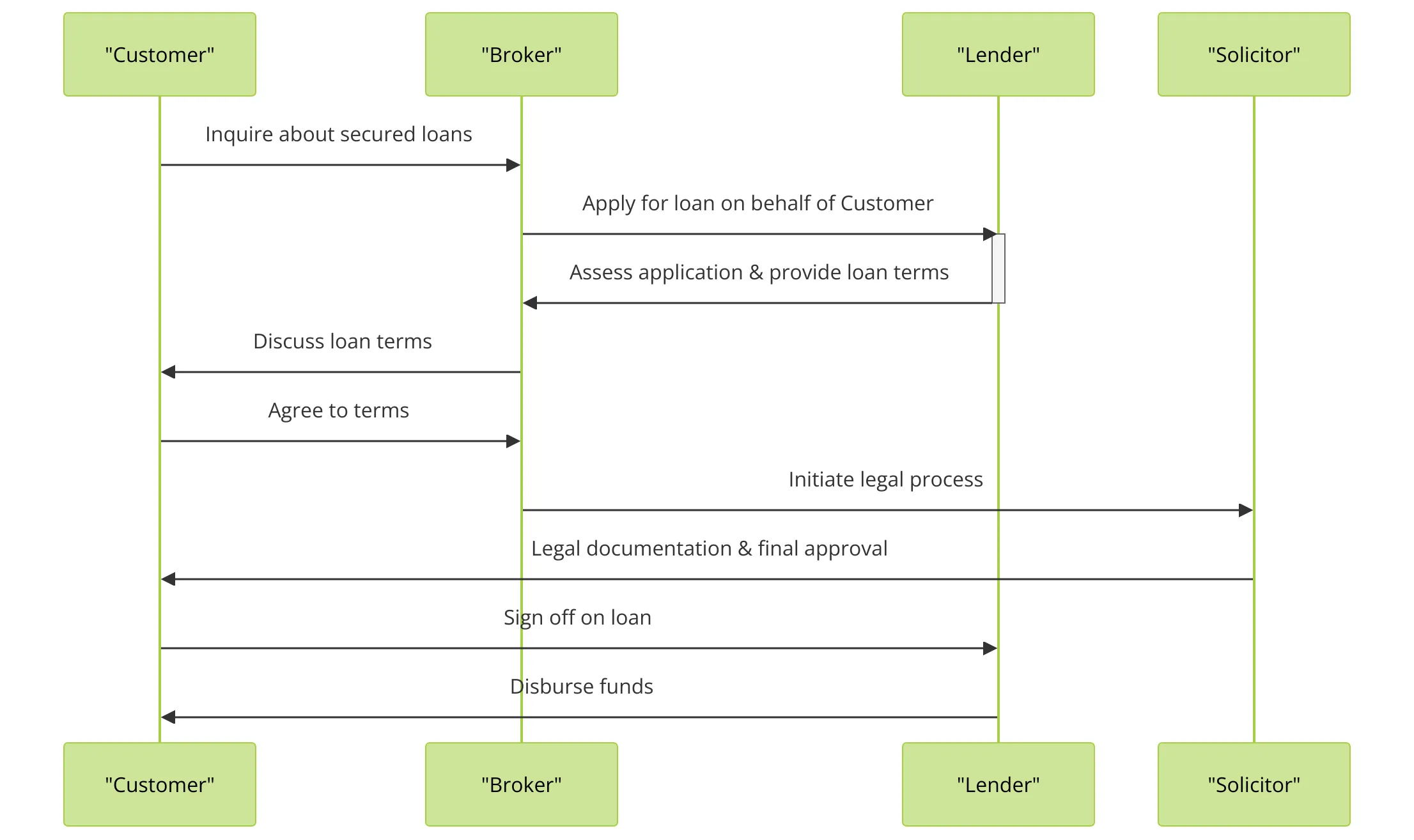

Secured loan broker process

Common secured loan questions

What are secured loans used for? In the UK, secured loans are frequently used for many reasons, including home improvements, extensions, debt consolidation and large purchases. A secured loan over 10 years may suit someone who wants a fixed period, while a £25,000 homeowner loan is more likely to be considered where there is sufficient income and home equity.

Do high-street names offer these loans? Some borrowers look at Lloyds, HSBC, RBS, Barclays, Santander, Nationwide, NatWest and TSB. A TSB secured loan may suit one borrower, while Santander home improvement personal loan options or Nationwide home improvement loans may suit another. Joint secured loans, and Natwest home improvement loans may also be worth comparing. Where credit history is poor, lenders such as Pepper Home Loans or Norton Home Loans may be more relevant than a prime bank.

Which specialist lenders are often discussed? Borrowers with unusual income or older credit issues may come across Masthaven Bank, Spring Loans, Paragon Bank, secured debt consolidation loans for bad credit, 1st Stop Loans Now Oplo, Optimum Credit, United Trust Bank, Precise Mortgages, Together Money Loans and the old Blemain name. The right one depends on the credit file, income, valuation and existing mortgage.

How does a credit score affect the deal? Some lenders care less about the score itself and more about affordability, recent arrears, gambling, payday loans, defaults, CCJs, and the amount of equity remaining in the property. A secured loan with no phone calls can work for people who prefer an online route, but the lender will still check the facts. It is also worth comparing the best rates available with slightly higher fixed rates if payment certainty matters.

Why do people look for no-broker bad-credit loans? Many people dislike paying a broker fee, especially if they already feel pressured by bills or missed payments. That is fair enough. The sensible test is whether the broker saves you time, protects your credit file from poor applications and finds a lender that you were unlikely to find on your own.